In the lack of some natural catastrophe, which can reduce the instant supply of homes, prices rise when need tends to outmatch supply trends. The supply of housing can also be sluggish to react to boosts in demand because it takes a very long time to construct or fix up a home, and in highly developed locations there simply isn't anymore land to build on.

Once it is developed that an above-average rise in real estate costs is initially driven by a need shock, we must ask what the causes of that increase in demand are. There are numerous possibilities: A rise in basic economic activity and increased success that puts more disposable income in customers' pockets and motivates homeownershipAn boost in the population or the demographic section of the population going into the real estate marketA low, general level of rates of interest, particularly short-term interest rates, that makes houses more affordableInnovative or new home mortgage products with low initial month-to-month payments that make homes more cost effective to new group segmentsEasy access to creditoften with lower underwriting standardsthat also brings more purchasers to the marketHigh-yielding structured mortgage bonds (MBS), as required by Wall Street financiers that make more home loan credit offered to borrowersA potential mispricing of threat by home loan lending institutions and home mortgage bond investors that expands the schedule of credit to borrowersThe short-term relationship in between a mortgage broker and a debtor under which borrowers are sometimes motivated to take extreme risksA lack of financial literacy and extreme risk-taking by home loan customers.

A boost in home flipping. Each of these variables can combine with one another to trigger a real estate market bubble to remove. Undoubtedly, these factors tend to feed off of each other. A detailed conversation of each runs out the scope of this article. We just explain that in general, like all bubbles, an uptick in activity and costs precedes extreme risk-taking and speculative habits by all market participantsbuyers, customers, lenders, contractors, and financiers.

This will take place while the supply of real estate is still increasing in action to the prior demand spike. Simply put, need reduces while supply still increases, resulting in a sharp fall in prices as nobody is delegated pay for much more homes and even greater prices. This awareness of risk throughout the system is activated by losses suffered by house owners, home loan lenders, mortgage financiers, and property financiers.

This typically results in default and foreclosure, which eventually adds to the present supply offered in the market. A downturn in general economic activity that causes less disposable income, job loss or less offered tasks, which reduces the demand for real estate (what is reo in real estate). A recession is especially unsafe. Demand is tired, bringing supply and need into equilibrium and slowing the quick rate of house price gratitude that some house owners, particularly speculators, depend on to make their purchases affordable or profitable.

The bottom line is that when losses install, credit requirements are tightened, easy home mortgage loaning is no longer readily available, need decreases, supply boosts, speculators leave the marketplace, and rates fall. In the mid-2000s, the U (what is redlining in real estate).S. economy experienced a prevalent real estate bubble that had a direct effect on causing the Great Economic downturn.

Unknown Facts About How To Get A Real Estate License In Texas

Low interest rates, relaxed financing standardsincluding extremely low deposit requirementsallowed people who would otherwise never ever have actually had the ability to acquire a home to become homeowners. This drove house prices up much more. However numerous speculative investors stopped purchasing because the risk was getting too expensive, leading other purchasers to get out of the marketplace.

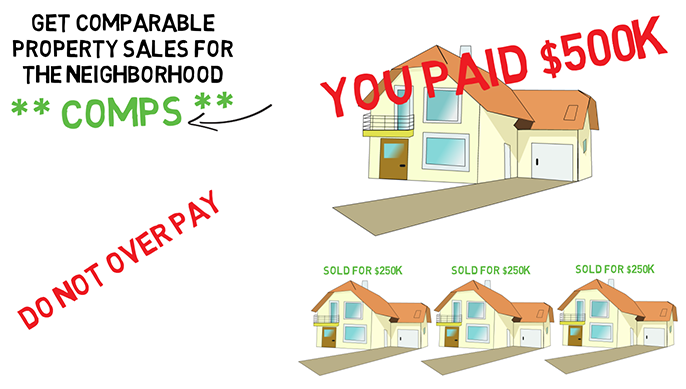

This, in turn, triggered rates to drop. Mortgage-backed securities were sold off in huge quantities, while home mortgage defaults and foreclosures rose to unprecedented levels. Too often, property owners make the harmful mistake of assuming recent rate performance will continue into the future without very first considering the long-lasting rates of price appreciation and the potential for mean reversion.

The laws of financing likewise specify that markets that go through durations of rapid rate gratitude or devaluation will, in time, revert to a rate point that puts them in line with where their long-term average rates of appreciation suggest they must be. This is called reversion to the mean.

After periods of quick cost gratitude, or in some cases, depreciation, they go back to where their long-lasting average rates of appreciation show they ought to be. Home cost suggest reversion can be either rapid or steady. Home rates may move rapidly to a point that puts them back in line with the long-lasting average, or they might remain constant until the long-lasting average overtakes them.

The calculated average quarterly portion increase was then used to the beginning worth displayed in the graph and each subsequent worth to obtain the theoretical Real estate Price Index worth. A lot of home buyers use just current cost efficiency as benchmarks for what they anticipate over the next several years. Based upon their unrealistic quotes, they take extreme threats.

There are a number of mortgage products that are heavily marketed to consumers and designed to be reasonably short-term loans. Customers choose these home loans based on the expectation they will be able to refinance out of that home loan within a certain variety of years, and they will be able to do so since of the equity they will have in their houses at that point.

Some Known Factual Statements About How To Get Into Commercial Real Estate

Property buyers need to aim to long-term rates of house price gratitude and consider the financial concept of mean reversion when making important financing decisions. Speculators should do the exact same. While taking dangers is not naturally bad and, timeshare offer in fact, taking threats is often required and recommended, the secret to making an excellent risk-based decision is to comprehend and determine the threats by making financially sound price quotes.

An easy and crucial principle of finance is mean reversion. While real estate markets are not as subject to bubbles as some markets, housing bubbles do exist. Long-term averages supply an excellent indication of where real estate rates will eventually wind up throughout durations of rapid gratitude followed by stagnant or falling rates.

Because the early 2000s, everybody from experts to experts predicted the burst of the. So, even participants on a game show might have problem quickly answering the question regarding the date. The bubble didn't in fact burst up until late 2007. Normally, a burst in the real estate market takes place in particular states or regions, but this one was various.

Generally, the housing market does reveal signs that it's in a bubble and headed for a little trouble (how to become a real estate broker in california). For example: Begins with a boost in demand The boost is paired with a limited supply of properties on the market Spectators, who believe in short-term buying and selling (referred to as flipping), enter the marketplace.

Need increases even more The marketplace goes through a shift. Need reduces or stays the very same as the real estate market sees a boost in supply. Prices Drop Click for more Housing bubble bursts The very same circumstance occurred leading up to late 2007. While the real estate market grew in the bubble, home was often costing overvalued costs from 2004 to the year prior to the burst.